Tax Insanity in the Golden State

California's Wealth Tax Proposal is Unconstitutional, Unworkable, and Economically Illiterate

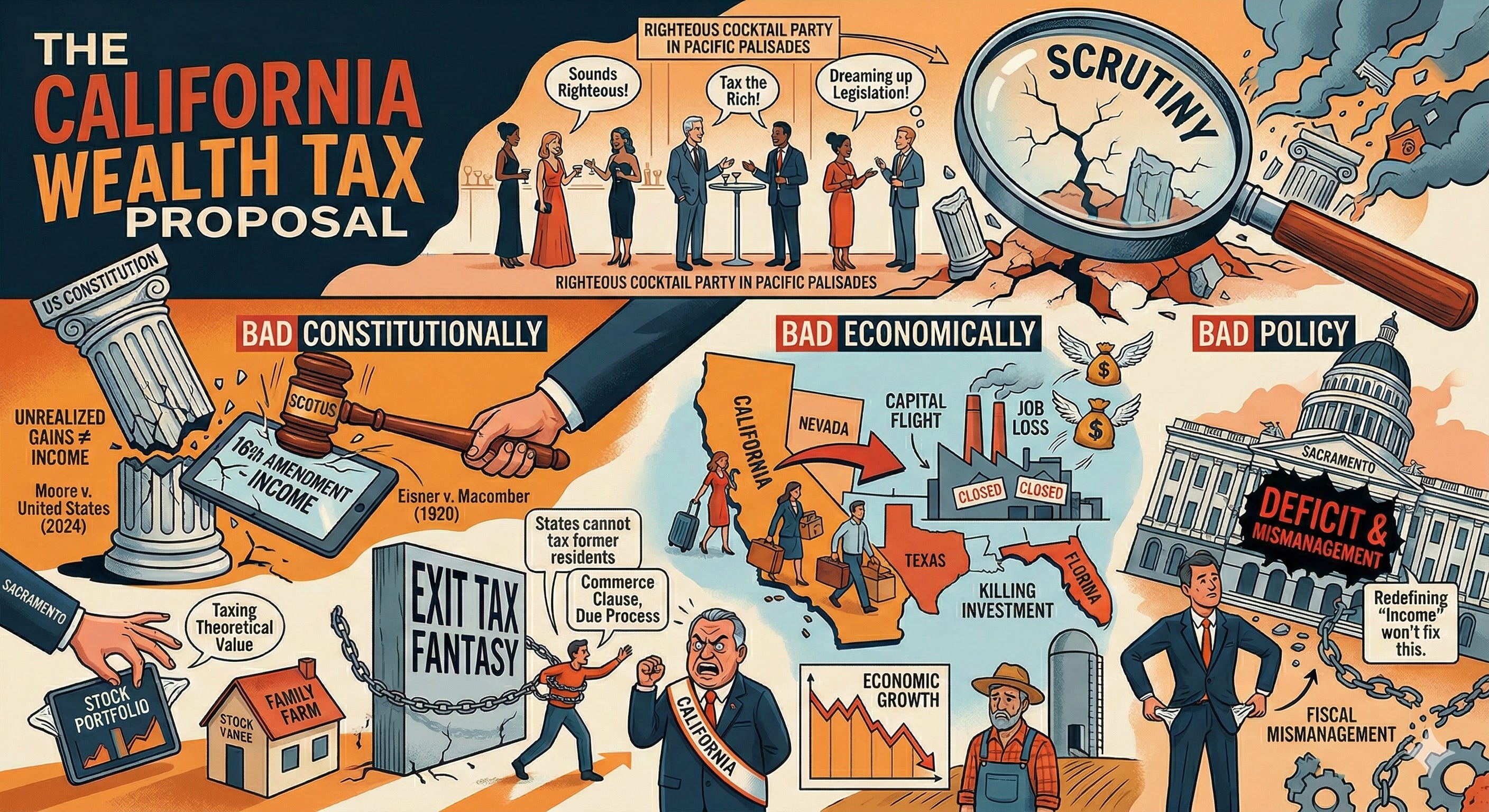

California has a recurring habit of dreaming up legislation that sounds righteous at a cocktail party in Pacific Palisades but falls apart the moment you expose it to scrutiny. The latest iteration o…

Keep reading with a 7-day free trial

Subscribe to The Duckpin to keep reading this post and get 7 days of free access to the full post archives.